The automated driving market is undergoing a significant shift, with a growing emphasis on scaling driver-assistance features that can be deployed across mainstream vehicle platforms. This shift is driven by the practical question of which automation level can be industrialised at volume, across regions, and within current regulatory and product-liability constraints.

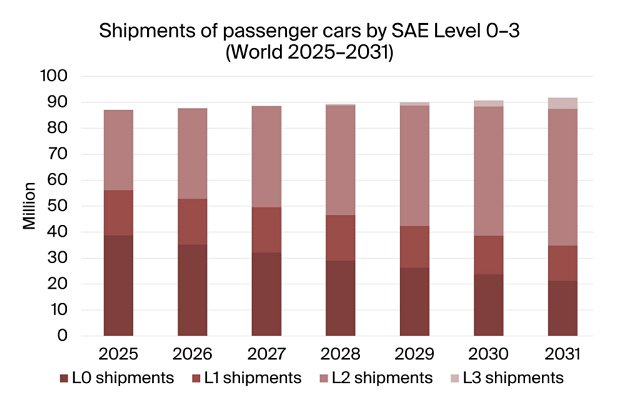

Berg Insight forecasts a sharp rise in automated driving penetration, with Level 2 systems expected in 57.3 percent of new cars sold globally by 2031. L2+ systems, a subset of Level 2 systems that adds more advanced assisted-driving functions, are also expected to play a significant role, with an estimated 31.0 percent of new passenger car sales featuring L2+ ADAS by 2031.

The most distinctive element in the forecast is the expected acceleration of L2+, which is expected to reach 28.4 million vehicles by 2031, up from 8.0 million in 2025. This represents a significant increase in the attachment rate, from 9.2 percent in 2025 to 31.0 percent in 2031.

The near-term automated driving market is being pulled toward driver-supervised systems rather than higher autonomy. Berg Insight expects only 4.8 percent of new cars sold in 2031 to feature Level 3 capabilities, while Level 4 passenger cars are not expected to scale in meaningful volumes before that year.

The emphasis has shifted from proving autonomy in limited domains to integrating sensors, compute, software, and user experience into systems that can be sold at scale while keeping the driver engaged. This creates a different deployment profile for OEMs, which are now prioritising the automation level that can be expanded more broadly across product portfolios.

Chinese OEMs are also playing a significant role in deploying sophisticated L2 and L2+ ADAS. Berg Insight identifies several leading Chinese players, including BYD Auto, Changan, Chery, Geely, GWM, Leapmotor, Li Auto, NIO, SAIC, and XPeng.

The report highlights the importance of advanced ADAS in the IoT and connected-vehicle ecosystem, which is driving increased integration pressure across the vehicle technology stack. OEMs need to align compute platforms, perception software, sensor choices, and map or localisation inputs, while system integrators and Tier 1s will be asked to package this complexity into deployable vehicle programs.

The forecast points to a market where commercial scale is likely to come from assisted driving rather than autonomy. For enterprises, fleet operators, and industrial players evaluating future vehicle platforms, the key takeaway is to look closely at the automation level being offered, not just the branding.

The mainstream automated vehicle will still largely be a supervised driving system by 2031, but one with a much more complex technology supply chain behind it. This has significant implications for the IoT and connected-vehicle ecosystem, as well as for the future of the automotive industry as a whole.