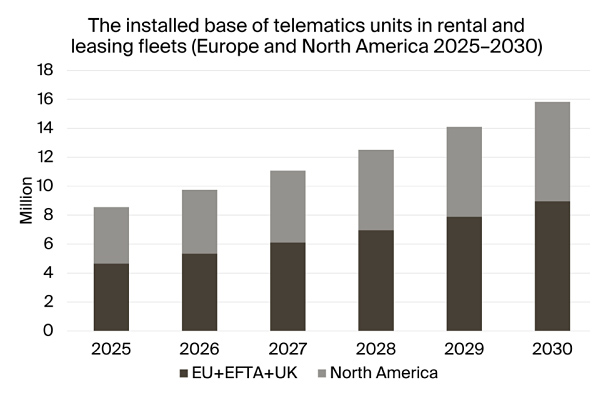

Telematics adoption in car rental and leasing fleets has accelerated, with active systems reaching 8.6 million units across Europe and North America by the end of 2025.

Industry forecasts indicate a compound annual growth rate of 13.1 % over the next five years, projecting the installed base to reach 15.8 million by 2030.

Fleet penetration is expected to climb from 56 % to 87 % in rental operations and from 49 % to 81 % in leasing operations over the same period.

The shift is driven by a move away from aftermarket devices toward data embedded by vehicle manufacturers, which reduces installation overhead but introduces integration challenges across diverse OEM platforms.

Operators must now focus on creating unified data layers that can harmonize information from multiple brands, enabling consistent workflow management across mixed fleets.

Telematics now supports a range of operational functions beyond simple location tracking, including theft prevention, misuse monitoring, utilization analytics, and the facilitation of contactless rental and car‑sharing services.

Environmental reporting is gaining prominence, with fleets using telematics to track CO₂ emissions and driver behavior, thereby meeting corporate sustainability and regulatory requirements.

Key technology providers in the space include Geotab, Targa Telematics, CalAmp, OCTO Telematics, Webfleet, Powerfleet, MySmartObject, Munic, Zubie, and RentalMatics, alongside mobility software and rental management platforms expanding into fleet use cases.

Vehicle manufacturers are increasingly monetizing embedded data for fleet customers, while connectivity providers face a market that values data integration as much as connectivity itself.

The overarching trend signals a transformation from isolated tracking solutions to integrated operational platforms that can process, normalize, and act on fleet data at scale.